German Chancellor, Olaf Scholz said in January that the government had successfully fended off the economic crisis, while the country’s minister of economy also addressed the extreme adaptability of German firms making it possible to avoid the worst scenarios. These statements strike a much more positive tone than those in October when negative growth was forecast for the German economy for 2023.

The panic over energy supplies has eased – at least for now – and the general outlook has significantly improved in the Germany, Austria, and Switzerland region (DACH) over the past 4 months. However, it remains clouded by some serious risks as the storms of disruption continues to rage above Europe. Organizations must remain cautious and stay focused on data to evaluate evolving risks and opportunities.

Business Risks are Hiding Behind Short-Term Improvements

The Russia-Ukraine War marks a critical economic and geopolitical turning point for Europe and the rest of the world – and the functioning of ICT markets has not escaped the impacts of the conflict.

Relying heavily on Russian gas, the DACH region has become particularly vulnerable to the increasing energy prices. Although the governments of Austria, Germany, and Switzerland reacted quickly to ensure energy supply for the winter months, the complete independence from Russian energy products is yet to come. Governments will have to consider that rapid escape from reliance on Russian gas may contravene with climate ambitions on the short term, therefore reducing energy demand and increasing energy efficiency will need to be in focus.

Although forecasts have been revised upwards during the past months, the latest data still indicate a major economic slowdown for the DACH region in 2023. Germany is expected to grow just 0.2%, while the economies of Austria and Switzerland are projected to see 0.5% growth. These numbers can easily go negative if geopolitical conflicts escalate or there is another major outbreak of COVID-19 in China, for example. Indeed, our Future Enterprise Resilience Survey found that more than 90% of German organizations expect recession this year.

DACH experienced the highest inflation in decades in 2022, and price increases are expected to weigh on households and businesses in 2023 and beyond. Switzerland is the only country in DACH, and one of only two countries in Europe, expected to keep inflation under 2% this year.

Labour shortage will be another major factor impacting IT budgets, while the lack of digital skills within the organization may hinder the completion of digital initiatives. Easing supply chain bottlenecks and declining transportation costs reduced pressures on some of the previously constrained sectors, such as automotive manufacturing, but the possibility of further supply chain disruptions cannot be ruled out.

How is the ICT market impacted by these headwinds and how should businesses approach weathering Europe’s storms of disruption?

Shifting Focus on Tech Investments

Despite volatile market conditions, ICT spending in the DACH region is expected to rise 4.9% this year and 6.4% over the 2021–2026 period, exceeding the European average. However, IT plans have been impacted. Organizations are reshuffling their investments, focusing on technologies that can sustain the growth in uncertain times, reduce costs, improve performance, optimize processes, enhance customer experience, and nurture talent.

Our identified the following key areas to drive ICT spending in the DACH region:

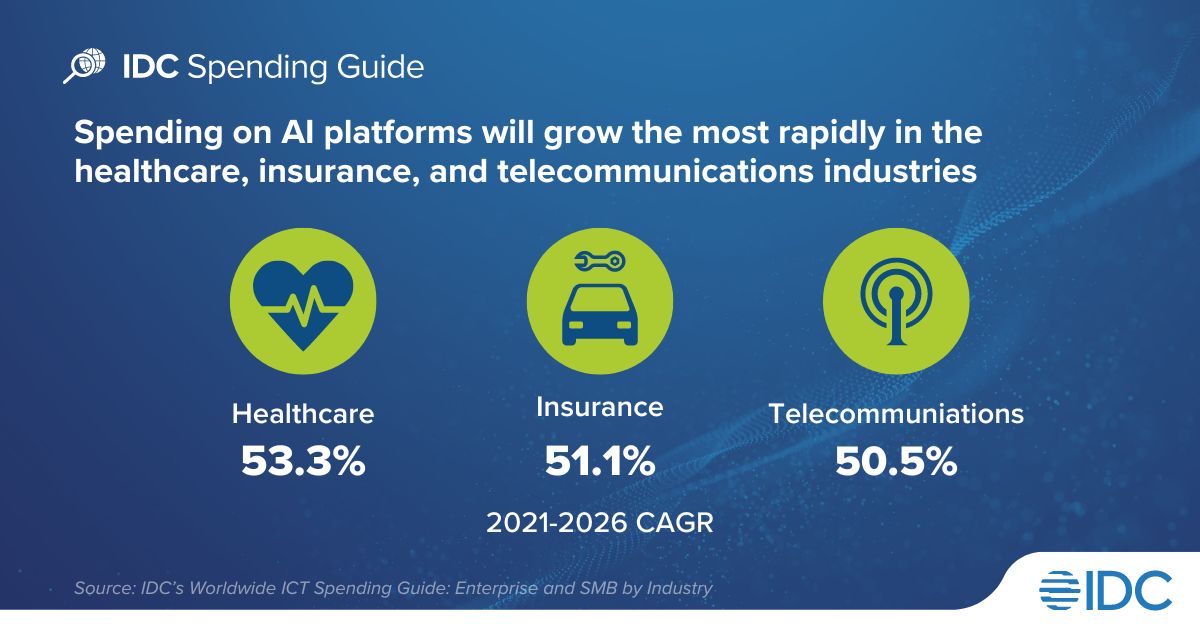

- Artificial Intelligence: AI’s tremendous potential to improve customer experience, enable new employee experiences, mitigate skills shortages, and transform the workplace is driving rapid adoption. Augmented human resources, image processing, fleet and freight management will be among the top 10 use cases related to AI. According to IDC’s Worldwide ICT Spending Guide: Enterprise and SMB by Industry, spending on AI platforms will grow an outstanding 46.6% in the DACH region during 2021–2026.

- Security: The rising frequency and sophistication of cyberattacks are keeping security a top investment priority. Annual spending on security in DACH is growing faster than the European average and is expected to exceed $18.5 billion in 2026.

- Cloud: Investments are expected to more than double between 2022 and 2026 as organizations continue migrating workloads and data to the cloud to boost cost efficiency, flexibility, and customer satisfaction.

- Internet of Things: IoT is a critical element of cost reduction, process optimization, and improved performance. Steady, double-digit growth in IoT spending is expected into 2026, with investments related to electric vehicle charging, advanced payments and shopping growing fastest.

Apart from these, enterprise infrastructure, managed services and project/professional services are additional areas where DACH organizations indicated they would continue their investment pace.

IDC’s Recommendations

Planning the IT budgets and identifying technologies to support growth in these uncertain times is extremely difficult, especially without having the right skills and partners to complete digital initiatives. In response to the current era of uncertainty, industries are embracing transformative new trends and technologies. Adapting to these transformations, being use case-centric, and placing the right bets for growth will be essential to keep afloat and continue delivering value.

IDC can help technology vendors stay resilient, competitive, and generate revenue during turbulent times. We offer the following assets to support organizations’ needs for precision planning:

- IDC Trackers enable organizations to assess their competition and their position by analyzing technology markets, vendor shares, and forecasts.

- IDC Black Books provide extensive market overviews to help organizations position their products and services for the appropriate audiences.

- IDC Spending Guides enable organizations to find strategic opportunities according to industry, company size, use case, and geography.

Contact us for more information about how IDC data products can help business leaders target, plan, and execute their most important strategic initiatives. We provide analysis of 100+ countries, 120+ technology markets, 20 industries, and 400+ use cases.