Challenges and Opportunities for the ICT Market in the Nordics

Navigating the Storms of Disruption in the Nordics — Finding Potential Beyond the Winds of Change

From the beginning of the pandemic, IDC has talked about the new winds of change that were to come and how to navigate them in a new normal context. Now, we are right in the middle of the change, and people, businesses, and society are enduring new storms of disruption, striving to find opportunities to keep afloat and continue to deliver value.

First the pandemic, and then the Russia-Ukraine war, have created a critical turning point for Europe and the entire world, impacting the functioning and evolution of global ICT markets, from tech demand and supply chain limitations to inflationary pressure, significantly increased costs of energy, skills availability, and increased cyberattacks. And Nordic countries have not been spared from the consequences of this situation, with the changing macroeconomic conditions resulting in a shift of business priorities. Customer satisfaction has remained ttop priority throughout the year, but cost savings have become relatively more important at the expense of profits.

According to the latest IDC Future Enterprise & Resiliency Spending Survey (FERS) from December 2022, more than half of Nordic companies find that rising IT costs have the greatest or second greatest impact on ICT spending plans. This is followed by challenges related to the IT supply chain and expectations of a coming recession.

IT investment plans are directly affected. When prices increase, companies need to either increase spending or reduce the amount purchased — e.g., buying fewer units, licenses, or consulting hours. While few markets are unilaterally impacted, the technologies and projects that have the strongest and most immediate impact on business performance fare better than the ones that can relatively easily be postponed.

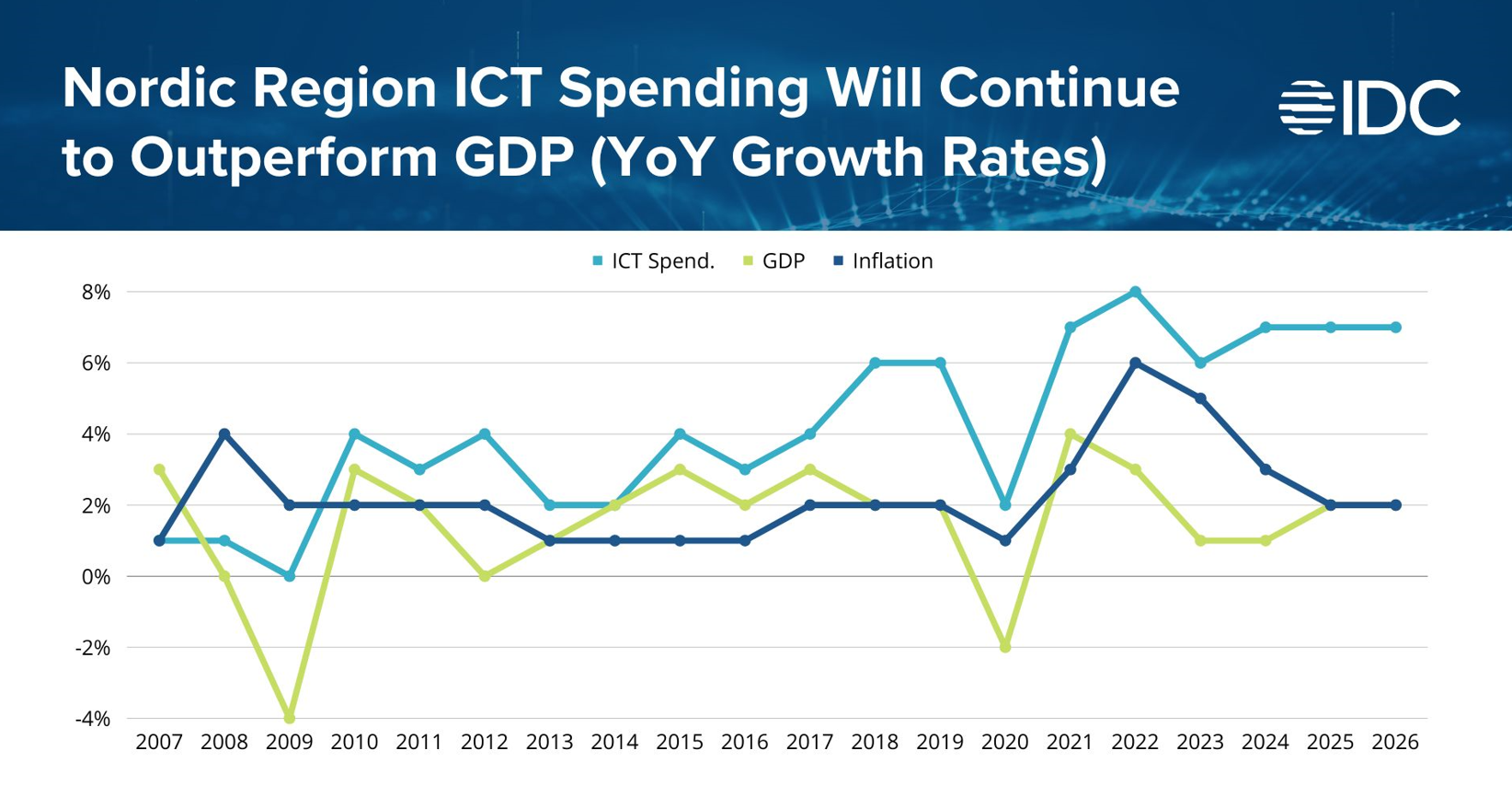

Despite the gloomy expectations, IT spending in the Nordic region, including Denmark, Finland, Norway, and Sweden, is expected to outperform GDP performance, as shown in IDC’s Black Book Live Edition from December 2022. However, with inflation expected to be around 5% in 2023, real growth will be limited.

Where Will Nordics Companies Expand Their Investments, Despite the Headwinds?

To maintain performance and mitigate the impact of the geopolitical and macroeconomic situation, Nordic companies will accelerate investments in technologies aiming to support them in their digital transformation.

Thus, the following key areas are identified by IDC to drive spending among Nordic organizations:

Cloud

Companies will keep their budgetary plans related to cloud infrastructure (IaaS) services. Overall cloud spending in the Nordics is estimated to achieve 22% five-year CAGR, reaching more than $27 billion by 2026. Even though more established than other emerging technologies, cloud will continue to drive investments across companies aiming to become digitally ready and to accelerate their business performance.

Internet of Things

According to the latest IDC European Emerging Technologies Survey from 2022, more than 40% of Nordic companies are already using IoT solutions. IoT is seen as part of the solution for the energy crisis, being critical to reduce costs, optimize processes, and improve performance. IoT spending will remain steady in Nordics, especially on use cases related to smart grids, electric vehicle charging, advanced payments, and so on.

Security

Investing in cybersecurity technologies is among the top 3 priorities for organizations in the next two years. Investment can be perceived as a cost center, but it also enables new offerings and reassures existing and potential customers. Cybersecurity spending in the Nordics is estimated to grow at 9% 5-year CAGR, reaching more than $6 billion by 2026.

Artificial Intelligence

Artificial intelligence is one of the fastest growing technologies due to tremendous potential to improve customer experience, enable new employee experiences, mitigate skills shortages, and transform the workplace environment. According to the latest IDC European Emerging Technologies Survey from 2022, more than 40% of Nordic companies are planning to adopt artificial intelligence solutions in the next two years.

Enterprise infrastructure, managed services, project/professional services, and anything “as a service” are additional areas where Nordic organizations indicated they will continue the pace of their investments.

How to Capture the Pockets of Growth in the Nordics Region

Many companies are struggling to find the right skills or partners to work with during the digital transformation journey, especially in such uncertain times. Offering guidance and support with the right technology stack, customized to address different industry-specific challenges will be the winning bet in these times.

To address all the challenges Nordic companies are facing, IT vendors must plan their strategy with precision. Adjusting to industry changes and rapid demand fluctuation, being use-case centric, and placing the right “growth” bets will be crucial to resist storms and headwinds.

IDC will help technology vendors remain resilient, stay competitive, and win revenue despite turbulent times by supporting their precision planning with the following assets:

- Assess your competition and your position by analyzing technology markets, vendor shares, and forecasts — IDC Trackers

- Position your products and services to the appropriate audience with an extensive market overview — IDC Black Book

- Find strategic opportunities by industry, company size, use case, and geography — IDC Spending Guide

Contact us for more information about how IDC Data products help business leaders target, plan, and execute their most important strategic initiatives, analyzing more than 100 countries, 120+ technology markets, 20 industries, and more than 400 use cases.

Winning the War for Talent with IT Service Cost Management

When organizations in all industries are struggling to attract talent, IDC explores opportunities for dealing with this shortage.

Introduction

Organizations in all industries are struggling to attract talent. The shortage of potential employees is a problem that has plagued the IT sector for years but has possibly never been worse than it is now. In this blog IDC explores opportunities for dealing with this shortage.

Employee Benefits

The most obvious perspective to consider is that of salary. Benchmarking employee expenses will allow your organization to match your peers and stop losing employees over salary competition.

Another benefit of benchmarking salary cost is tackling the possible internal tug of war for budget increases. An independent benchmark report is often useful to convince senior management that additional budget is required, if the benchmark points this out.

However, employees are not motivated by salary alone. For many, satisfaction also comes from working on cutting-edge technology, something that only some IT organizations allow an employee to do. In contrast, maintaining legacy systems at less competitive organizations may not be interesting to IT professionals who love to experience technology. In a benchmark, the technologies maintained by the IT staff are closely examined and compared to peers. IDC identifies key areas to innovate your business’ digital transformation, keeping IT staff engaged at the same time.

Optimize Your Current Environment

Another perspective to take is optimizing the existing situation. If finding new IT talent is challenging, IT management must consider ways to maximize the use of existing employees. With talent being as scarce as it is, management must be fully aware of possible optimizations.

A benchmark will show how teams are performing in terms of productivity and where potential exists.

Because IDC’s data collection methods dive deep into your IT administration and governance, gaps that no doubt exist are discovered and reported on. The results of a benchmark will uncover where your automation is lacking and whether your end users are educated to market conform levels. All of these insights will allow you to deliver more and better IT with the resources that you already have available.

Rationalizing and consolidating your IT environment has many benefits and generally offers an attractive business case. That said, possibly the most interesting result is simply reducing the amount of IT that needs to be managed by the talent that is so scarce. The size and complexity of the IT environment is a large factor in our benchmarks, be it the complexity of the networks, the size of the datacenter services, the setup of the end user workplace, or the amount of contract management and governance required. IDC reports on all of these components and shows the way to reducing unnecessary complexity and size.

Is Outsourcing the Way?

Finally, if the options of increasing budgets, optimizing teams, and reducing complexity are exhausted, outsourcing more of the IT services can be considered. Outsourcing can be a relatively quick answer to a suboptimal internal IT team, but it does not come without its share of challenges. The first step is deciding which IT domains are attractive candidates to place under a contract. In other words, an organization needs a sourcing strategy. This strategy will determine how each part of the IT organization should be sourced and what a fitting roadmap to get there should look like. Prioritization of rationalization projects are also considered, as well as the potential to supplement existing teams with external talent from an IT supplier.

Cost is, of course, an important factor in deciding which sourcing scenarios are feasible for the organization. IDC will provide so called ‘landing zones’ in which the future cost of a sourcing scenario are modeled based on the current IT market. This is essentially a virtual benchmark of your IT organization as if parts of it were outsourced.

If IT is outsourced in some way, the existing organization should also change. External contract governance and service management capabilities need to evolve and a future organizational model needs to be constructed. When transforming the organization, one must also consider whether it is attractive to re-educate the existing teams into roles that are needed in the new organization.

The ongoing war on talent is challenging. This blog, however, has hopefully shown that the tools to navigate this challenge exist. IDC continues to help organizations daily and to us, the current market offers new and exciting ways to help CIOs globally.

Interested in diving deeper into IT Service Cost Management? Check out our infographic.

Can’t wait until the next blog is published to learn more about cutting cloud costs? Contact us to schedule a conversation.

The Future Generative AI Tool That I Would Like

Generative AI is the buzzword of the day. More specifically, ChatGPT, the OpenAI model that is trained to interact in a “conversational way”.

The dialogue format enables ChatGPT to answer follow-up questions, admit its mistakes and challenge incorrect premises. Of course, like many geeks in the ICT industry and beyond, I have tried it.

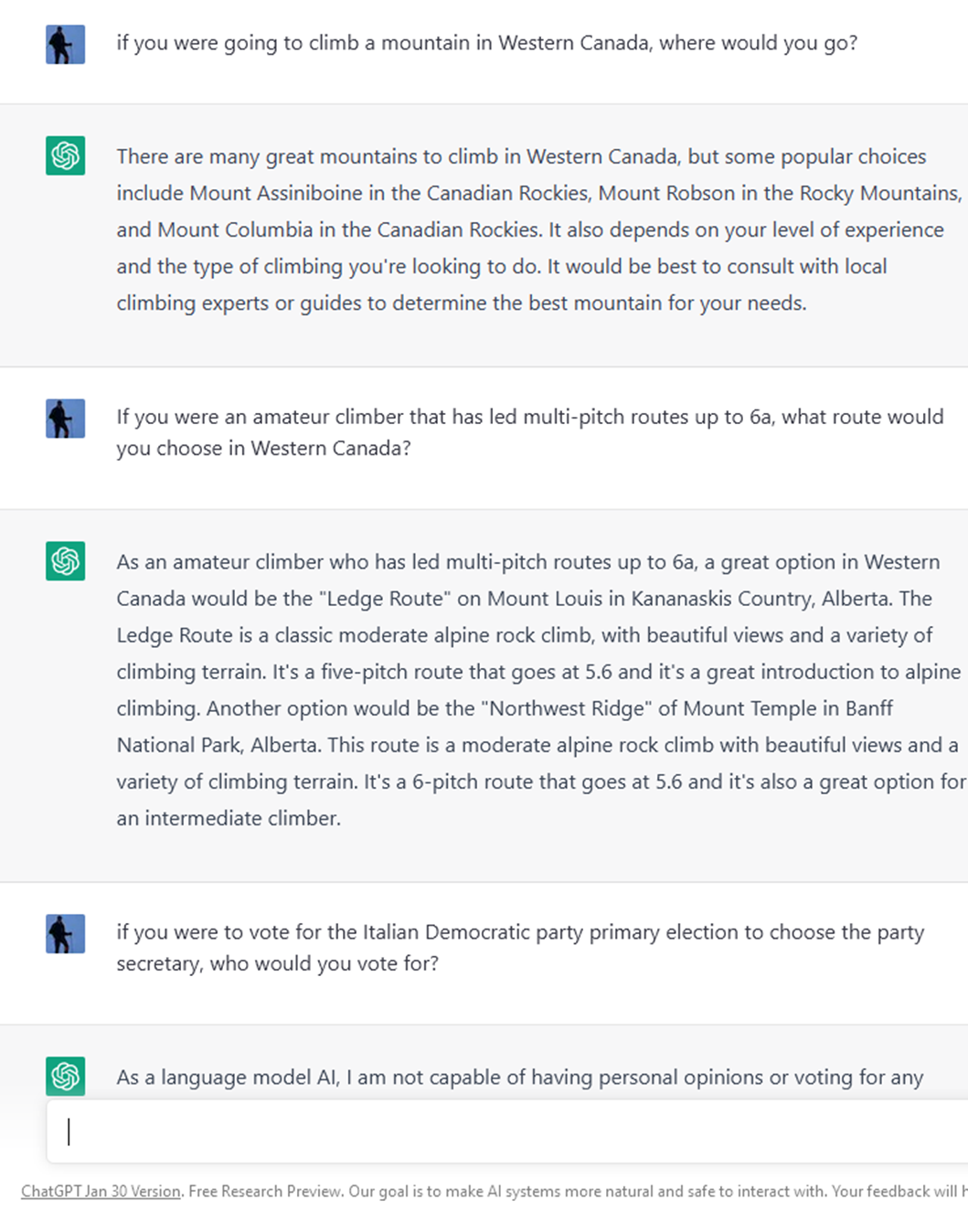

It’s quite impressive. Well, besides the fact that it took me a couple of attempts to find the right time of the day when traffic was not so high to cripple access. I asked a couple of questions about my passion, mountaineering and climbing.

The answers were correct, although a bit conservative. For example, when I asked about which multipitch routes I could climb with my level of experience, in Western Canada, the model provided only two options that were exactly in line with my multipitch skills. Instead, I would have appreciated a wider variety of options, some easier and some harder than my skill level, so that I could make a choice.

The model also told me to consult local guides for more information, which indicates that careful ethical principles, like personal safety, are embedded in the design of the algorithm. I then asked about who I should vote for in the upcoming primary to elect the new secretary of the Italian Democratic Party. The answer was that the model can’t express a political opinion, but that it could provide me with the list of candidates.

That’s fair enough, and further proof that ethics are taken into account. So, I asked for the list of candidates and their programmes. The answer was that the model is trained on historical data available until 2021, so it’s not up-to-date on events between 2022 and early 2023. This is understandable, but I would expect it to be quasi real time in the future.

Regardless, fascinating.

Embracing the Augmentative AI Vision

I’ve not done enough research (yet) to say how good the model is and for what use cases. Many of my IDC colleagues are developing thought-leadership research and collecting in-depth data into how generative AI will affect enterprise and consumers.

What I’m thinking about is the societal implications of generative AI. This was triggered yesterday during our first meeting with the 2023 IDC Government Xchange Advisory Board. Gwendolyn Carpenter, a member of the Advisory Board, who has kids in school, said she’d heard about students using it to cheat on their homework.

My colleague Matt Ledger has already written a quick take on this matter too. As Matt noted in his piece, there are a range of opinions on this, from schools that believe ChatGPT can be very valuable as a learning tool, to those that are uncertain about the impact and have temporarily banned usage, to educators that believe that generative AI could make redundant our ability to write, learn and eventually think. This, paradoxically, could hamper our ability to invent brilliant new tools such as ChatGPT itself.

I am no Luddite. I don’t think we should stop progress. But I think generative AI is a great case in point for the ongoing debate about whether we should design AI that can replace human abilities versus AI that can augment human abilities.

For example, I don’t want generative AI to replace my writing, just because it’s much faster and more elegant than I am at synthesising available knowledge. I’m having a lot of fun expressing my opinions in this blog because, in a way, I’m creating it while I write it!

But I would definitely like to have a tool that can critique my writing. A tool that could, for instance, highlight where my piece is biased or where I could consider additional sources of data and literature to enrich my perspective. Sort of a much smarter version of the spell checker that tells me if there’s a typo or if I didn’t use punctuation correctly or if I used too many passive forms. This augmentative AI tool would push my brain to think more, not less. And I’d still be able to make my own choices on whether to apply the advice or not.

Policymakers need to think about how they can shape the new norms to maximise the benefits and tackle the risks of AI. For instance, by recommending (or mandating) a machine-readable label that helps recognise if a piece of content is generated by AI, for example in the case of government-regulated certifications. But regulation is not enough.

If that does not happen, AI will fail to meet the high expectations that it can be a positive force in the future. In fact, according to our Future Enterprise Resilience and Spending Survey (Wave 11, December 2022), only 25% of government executives worldwide think the promise of AI has completely lived up to their organisation’s expectations.

The future of generative AI (and the AI market in general) will depend on whether users and suppliers embrace the human augmentation narrative, in both the B2B and B2C worlds. We need to ask ourselves what kind of AI solutions we want — solutions that replace humans or augment humans. And then design and engineer them in a way that reflects that purpose.

I look forward to discussing more about the power of innovation, and how we can use it at scale to make a positive and ethical impact on society, at our Government Xchange.

Key Insights from NRF 2023: Mastering the Foundations to Get Ready for What's Next

In a chilly and wintery New York, the IDC Retail Insights team joined more than 30,000 attendees from technology and retail companies at Javits Convention Center for NRF 2023: Retail’s Big Show. The four-day event, which took place from January 14 through January 17, was the first since the pandemic, and everyone was excited to meet in person after two years of remote interactions.

We attended more than 150 meetings with technology vendors to learn more about their offerings and discuss the latest trends in retail technology.

Here are some of the key points from our conversations:

In-store Frictionless Experience, Next-generation Checkouts

The physical store is making a big comeback, and this was visible when browsing the floor at NRF. Customer expectations have changed in the past few years and the store can no longer operate as before.

The challenge for retailers is how to “modernise” store visits and minimise friction. Vendors are expanding their offerings to accommodate this. We saw numerous innovative solutions to make checkout frictionless, including biometric checkout (through palm scanning or face recognition), POS leveraging IoT and computer vision to recognise products and improve loss prevention, and walk-out solutions.

eCommerce-like Experience In-store and Online-offline Integration

Reinventing the POS is part of a broader narrative focusing on the digitalisation of the physical store experience and online-offline integration. Computer vision and IoT in POS, for example — aside from making it easier for shoppers to pay in-store and prevent losses — effectively connect the front end (the POS) with the back-end operations (e.g., inventory management) for better omni-channel experience and operation management. In addition, shoppers expect greater, ecommerce-like engagement in the store, such as scanning a product to gather more information like customer reviews and item features.

Payments

Payment capabilities are becoming increasingly important in retail operations, particularly with the expansion of digital commerce and omni-channel retail. We noticed how some providers were announcing new payment platform offerings and new partnerships in the area.

As for in-store checkouts, digital payment can create friction if not executed well. With the proliferation of payment types available to shoppers and regional differences in terms of preferred methods, retailers need to ensure they can offer a vast range of options.

Also, payments need to connect with the entire customer journey and its personalisation options, such as shoppers linking to their loyalty schemes or donating to their preferred charity when checking out.

Reverse Experience

There is a growing emphasis on the back-office operations that are instrumental in retailers providing great omni-channel customer experience. In conjunction with the importance of front-end customer journey personalisation, what’s behind the scenes becomes key to meeting the expectations of increasingly channel-agnostic shoppers. Reverse experience — improving operational efficiencies to provide great customer journeys — is one of the key themes of our research for 2023 (watch this space!).

One vendor told us that order management systems (OMS) are the powerhouse that enable omni-channel retail. We agree. Among back-office operations, logistics and fulfilment weigh on retail operations’ profitability.

In addition, staff shortages make it harder for retailers to expand in the area. During our conversations at NRF, we came across concepts such as automation in fulfilment (e.g., microfulfilment), democratisation and uberisation of last-mile fleets (joining forces with partners to expand last-mile delivery), and solutions for reverse logistics and returns minimisation.

Employee Engagement

Reverse experience also means focusing on people — not just the customers but also employees and how store associates can integrate the two sides of the shopping experience to offer the best customer experience leveraging the right instruments, tools and training. The role of the store associate is growing in conjunction with the pivotal role of brick-and-mortar retail in the post-pandemic omni-channel environment.

Immersive Experience

Customers expect a coherent and augmented shopping experience. This should have the power (and the mystery) to transcend any discrepancies across channels.

Visual commerce is already a reality for retailers and brands that aim to enhance 360-degree customer engagement. This includes 3D visualisation, live streaming shopping, product design, digital showrooms, virtual try-on, the creation of personalised digital objects, virtual shopping assistants, customer care agents and human-like generated content.

Data Management

Customer data remains the fuel of the retail and consumer industry. Customer data platforms (CDPs) and data lakes have been the engine for collaboration between retail peers and brands. At the same time, AI and ML analytics are the foundational elements that convert data into actionable insights, that are converted into a better customer experience and personalisation, data accuracy, data security, identity management, data privacy and regulatory compliance, and data valorisation within partners’ ecosystems to generate a new source of revenue streams (e.g., retail media networks).

Loyalty

Retailers always aim to increase and maintain loyalty to build solid and trusted relationships with clients. This has led retailers to mix and match loyalty schemes, moving beyond rewards and unlocking customer lifetime value.

The platform-based approach to loyalty capabilities that we heard about in several conversations throughout the event is a clear sign that both retailers and brands have realised how important loyalty and customer satisfaction have been, especially during the pandemic. This has raised the bar for customer expectations and has led to new forms of collaboration between brands, as in the case of delivery subscriptions, by combining convenience, personalisation and omni-channel.

Next-generation Retail Platforms

Commerce platforms are central to retailers’ technology stacks. Retailers and D2C brands are looking for agility and flexibility in their commerce architecture to achieve omni-channel-ready operations.

These were recurrent topics in our conversations with commerce platform providers during the event. Composability was the key feature of next-generation commerce platforms at NRF. Composable commerce enables merchants to combine business services or modules without affecting other parts of the architecture. Simplifying UX and reducing the cost of experimentation are key objectives of the next-generation commerce architectures we came across at NRF, as well as enabling plug-and-play capabilities by ensuring the readiness of the back-end interface, such as making product categorisation ready for use in different touchpoints with the shopper, including mobile commerce apps and social media apps such as TikTok.

Retailers are focusing on getting the foundational capabilities right to meet the requirements of an increasingly complex omni-channel environment, particularly as the physical store is again becoming the centre of omni-channel operations and there is a strong need to blend online and offline and make the brick-and-mortar experience more digital. This resonates well with the reverse experience narrative.

Themes that would probably have been more prominent during the pandemic, including the role of emerging technologies such as blockchain, NFTs, Web3 and the metaverse, were less visible this year. We don’t believe retailers are turning their back on more visionary topics, however. Rather, they are preparing their back-end operations for the future of retail — whatever form that might take.